Contact us For Bank Of England

Introduction Mortgage Interest Rates in the UK

In the ever-evolving landscape of the UK housing market, one of the most crucial factors that potential homeowners and investors consider is mortgage interest rates. These rates not only dictate the cost of borrowing but also significantly influence the affordability of homeownership and the overall health of the real estate sector. As we step into 2024, it’s imperative to examine the current state of mortgage interest rates in the UK and explore the factors shaping them.

Mortgage Interest Rates in the UK

Understanding Mortgage Interest Rates:

Mortgage interest rates represent the percentage of the loan amount charged by lenders to borrowers for the privilege of borrowing funds. These rates can vary based on several factors, including economic conditions, inflation rates, central bank policies, and market competition among lenders. Generally, lower interest rates encourage borrowing and stimulate housing market activity, while higher rates can dampen demand.

Current Trends in UK Mortgage Interest Rates:

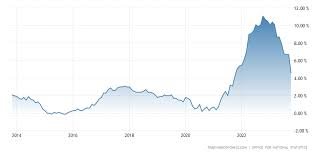

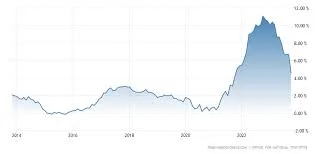

As of 2024, the UK mortgage market continues to witness historically low interest rates, albeit with some fluctuations influenced by both domestic and global factors. The aftermath of the COVID-19 pandemic, ongoing economic recovery efforts, and the Bank of England’s monetary policies all play a significant role in shaping mortgage rates.

Mortgage Interest Rates in the UK

The Bank of England’s Base Rate: The Bank of England’s base rate, often referred to as the “Bank Rate,” serves as a benchmark for various interest rates in the UK financial system, including mortgage rates. Throughout 2023 and into 2024, the Bank of England has maintained a cautiously accommodative stance, balancing the need for economic growth with concerns over inflationary pressures. Any adjustments to the base rate by the Bank of England can have a ripple effect on mortgage rates offered by lenders.

Impact of Economic Indicators:

Several economic indicators influence mortgage interest rates in the UK. Key factors include inflation rates, employment figures, GDP growth, and consumer spending patterns. Inflationary pressures, in particular, can drive central banks to adjust interest rates to maintain price stability. Additionally, changes in employment levels and wage growth impact consumers’ ability to afford mortgage repayments, thus influencing demand for loans.

Mortgage Interest Rates in the UK

Global Economic Environment:

The interconnectedness of the global economy means that events and trends abroad can also affect mortgage interest rates in the UK. Factors such as geopolitical tensions, trade dynamics, and monetary policies of major economies like the United States and the European Union can impact global financial markets, leading to fluctuations in interest rates.

Government Initiatives and Housing Policies:

Government initiatives and housing policies also play a crucial role in shaping mortgage interest rates and housing market dynamics. Programs aimed at stimulating homeownership, such as Help to Buy schemes or initiatives to increase housing supply, can influence demand for mortgages and subsequently impact interest rates. Additionally, regulatory changes and tax policies related to property ownership may affect investor sentiment and lending practices.

Lender Competition and Product Offerings:

Competition among mortgage lenders remains fierce in the UK market, with institutions vying to attract borrowers through competitive interest rates and product offerings. While traditional high street banks continue to dominate the mortgage landscape, digital banks and non-bank lenders have gained traction, introducing innovative mortgage products and services. This competitive environment can lead to greater choice for consumers but also requires borrowers to carefully compare rates and terms before selecting a mortgage provider.

Mortgage Interest Rates in the UK

Forecast and Considerations for Borrowers:

Looking ahead, the trajectory of mortgage interest rates in the UK for the remainder of 2024 remains subject to various uncertainties, including the path of economic recovery, inflationary pressures, and central bank policies. While rates are likely to remain relatively low compared to historical norms, potential borrowers should stay vigilant and monitor market developments.

For prospective homebuyers, securing a mortgage involves more than just finding the lowest interest rate. Factors such as loan terms, repayment options, and overall affordability must be carefully considered. Moreover, borrowers should assess their financial situation, long-term goals, and risk tolerance before committing to a mortgage.

Conclusion:

Mortgage interest rates in the UK for 2024 reflect a complex interplay of economic, regulatory, and market forces. While the prevailing low-rate environment offers opportunities for homeownership and investment, borrowers must navigate the landscape with careful consideration and informed decision-making. By understanding the factors influencing mortgage rates and staying attuned to market dynamics, individuals can make sound financial choices aligned with their housing goals and aspirations

Mortgage in Principle in the UK

FAQ: Mortgage Interest Rates in the UK for 2024

What are mortgage interest rates?

Mortgage interest rates represent the percentage of the loan amount charged by lenders to borrowers for borrowing funds to purchase a property. These rates can vary based on economic conditions, central bank policies, and market competition among lenders.

What are the current trends in UK mortgage interest rates for 2024?

As of 2024, the UK mortgage market continues to experience historically low interest rates. However, these rates may fluctuate due to factors such as economic recovery efforts, inflation rates, and monetary policies set by the Bank of England.

How do economic indicators influence mortgage interest rates in the UK?

Economic indicators such as inflation rates, employment figures, GDP growth, and consumer spending patterns can impact mortgage interest rates. Central banks may adjust interest rates to maintain price stability in response to inflationary pressures or changes in economic conditions.

What role does the Bank of England play in determining mortgage interest rates?

The Bank of England’s base rate, often referred to as the “Bank Rate,” serves as a benchmark for various interest rates in the UK financial system, including mortgage rates. Changes to the base rate by the Bank of England can influence borrowing costs for consumers.

How do global economic factors affect mortgage interest rates in the UK?

Events and trends in the global economy, such as geopolitical tensions, trade dynamics, and monetary policies of major economies, can impact global financial markets. These developments may lead to fluctuations in mortgage interest rates in the UK.

What impact do government initiatives and housing policies have on mortgage interest rates?

Government initiatives aimed at stimulating homeownership or increasing housing supply, as well as regulatory changes and tax policies related to property ownership, can influence demand for mortgages and affect interest rates.

How does lender competition influence mortgage interest rates in the UK?

Competition among mortgage lenders in the UK remains fierce, with institutions offering competitive rates and product offerings to attract borrowers. This competitive environment can provide consumers with greater choice but requires careful comparison of rates and terms.

What factors should borrowers consider when evaluating mortgage options?

When evaluating mortgage options, borrowers should consider not only the interest rate but also loan terms, repayment options, overall affordability, and their own financial situation and long-term goals.

Can borrowers predict future changes in mortgage interest rates?

While borrowers cannot predict future changes in mortgage interest rates with certainty, staying informed about economic indicators, central bank policies, and market trends can help them make informed decisions about mortgage financing.

How can borrowers secure the best mortgage interest rates in the current market?

Borrowers can secure the best mortgage interest rates by comparing offers from multiple lenders, maintaining a strong credit score, providing a sizable down payment, and demonstrating stable employment and income. Additionally, seeking pre-approval can help borrowers negotiate favorable terms with lenders.